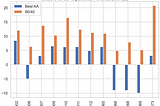

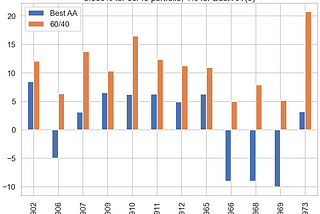

EREVNHow important is asset allocation versus withdrawal rates in retirement?I have this intuition that withdrawal rates are far more important than asset allocation. Whether you withdraw 3% versus 4% is far more…8 min read·May 31, 2020--1--1

EREVNThe (Fading) Power of DividendsYou’ve probably heard talk about the key role that reinvesting dividends play in total returns.4 min read·Apr 30, 2020----

EREVN“Can Low Retirement Savings Be Rationalized?”I’ve long been dubious about the hand-wringing around retirement savings in America. There is certainly room for improvement but I’ve never…3 min read·Mar 4, 2020----

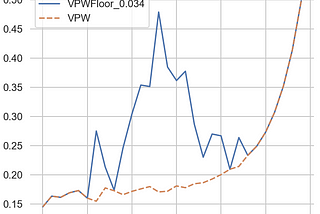

EREVNinThe StartupAdding a floor to variable withdrawals.Variable withdrawal schemes can often see us cut our withdrawals dramatically in retirement. It is tempting to add some kind of floor — a…10 min read·Mar 2, 2020--1--1

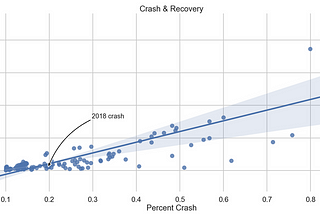

EREVN“Data science” and the 2018 stocrash & recoveryThis is more of a “look how easy pandas & friends make it to investigate things” than anything fully baked. Close to a tutorial than…5 min read·Jan 21, 2020--1--1

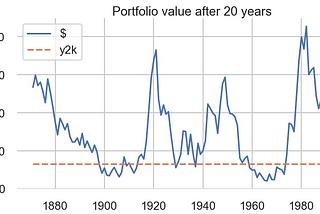

EREVNYear 2000 Retirement: a 4% SWR Reality Check (3rd edition)In 2017 I wrote the second edition, updating how a Year 2000 retiree has actually done.2 min read·Jan 2, 2020----

EREVNLowering sequence of withdrawals risk by living abroad and the craziness of Safe Withdrawal Rate…One widely known, but little discussed, aspect of the 4% rule is that is has a severe flaw around timing of retirement.5 min read·Dec 22, 2019----

EREVNOptimal lazy rebalancing“Optimal lazy rebalancing” is a technique that Albert H. Mao wrote an online calculator for a number of years ago.2 min read·Dec 21, 2019----

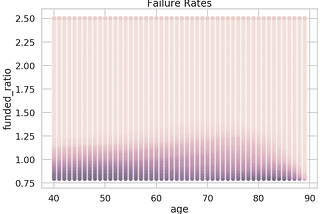

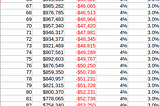

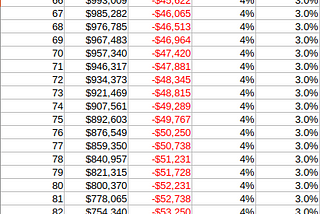

EREVNConnecting Funded Ratios and Success RatesI think the Funding Ratio is a pretty great tool for retirement planning. It can easily take into account your entire balance sheet —…6 min read·Nov 26, 2019--1--1

EREVNBlanchett’s “spending smile” and PMT ratesWhen we use the PMT calculation to guide our retirement planning, we need to pick a “rate” as one of the parameters. What that rate should…6 min read·Nov 24, 2019--1--1